Understanding the difference is crucial for F&O traders because it directly impacts tax treatment, loss adjustment, and audit applicability.

Speculative Income

Speculative Income

- Arises from transactions where actual delivery is not intended

- Example: Intraday equity trading

- Governed under Section 43(5)

- Loss Set-off: Can be set off only against speculative income

- Carry Forward: Allowed for 4 years only

- Tax Treatment: Considered high-risk and restricted for adjustments

Non-Speculative Income

- Arises from business activities including F&O trading

- F&O is treated as non-speculative when traded on recognized stock exchanges

- Loss Set-off: Can be set off against any income except salary

- Carry Forward: Allowed for 8 years

- Tax Treatment: Treated as normal business income with broader benefits

Key Differences at a Glance

| Basis | Speculative Income | Non-Speculative Income (F&O) |

|---|---|---|

| Nature | High-risk, no delivery | Business income |

| Example | Intraday trading | Futures & Options trading |

| Loss Set-off | Only against speculative | Against any (except salary) |

| Carry Forward | 4 years | 8 years |

| Tax Flexibility | Limited | More flexible |

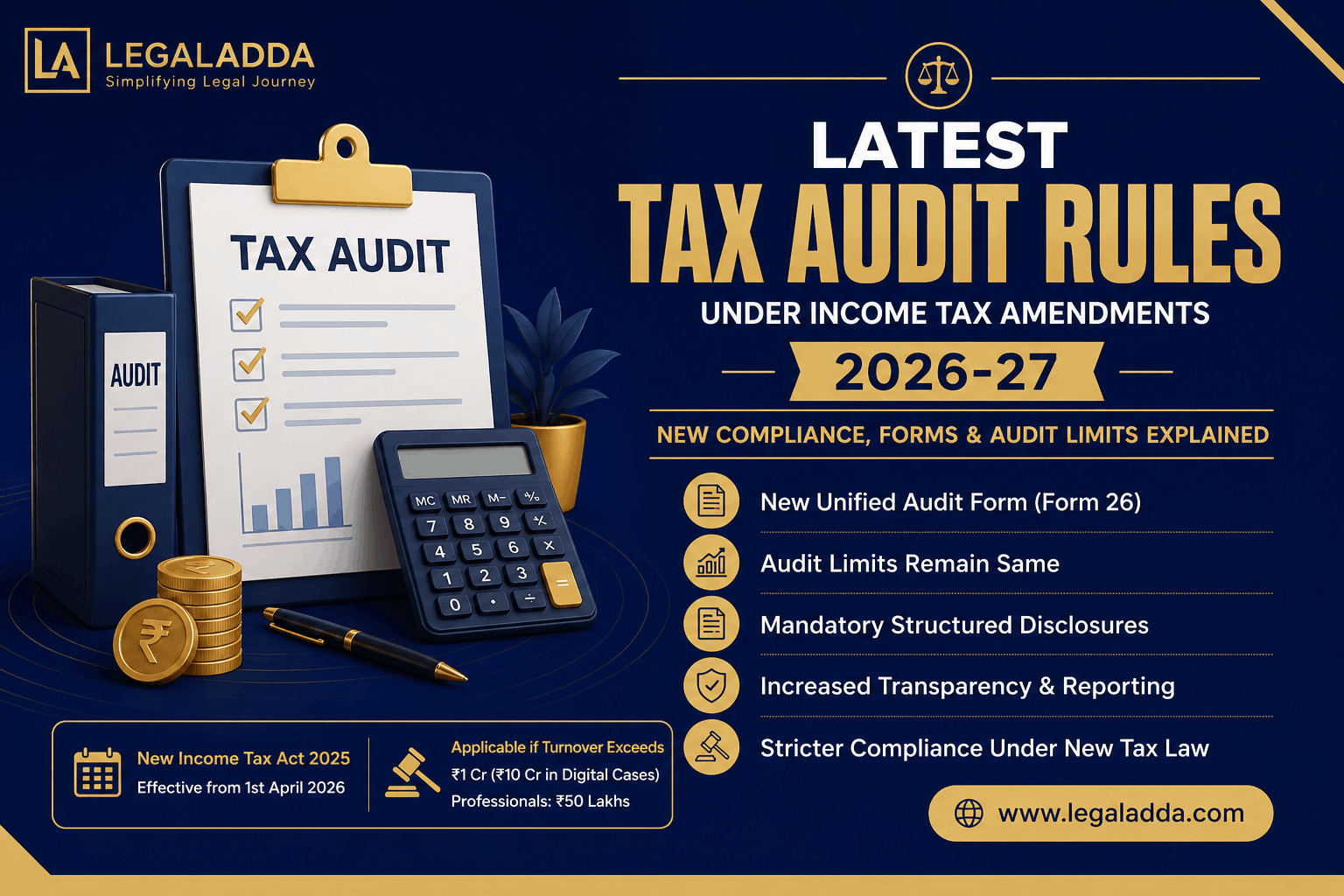

Increased Thresholds

- Basic tax audit limit remains ₹1 crore

- Limit extended up to ₹10 crore for digital transactions

- Applicable only if cash transactions ≤ 5% of total receipts & payments

- Reduces audit burden for high-volume digital traders

Digital Transaction Consideration

- Strong focus on cashless / digital trading

- Higher audit limit available for online trading transactions

- Encourages use of banking channels & proper records

- Helps in better transparency and tracking of income

Compliance Updates

- Mandatory to maintain proper books of accounts

- Turnover must be calculated as per ICAI guidelines (P&L method)

- Timely filing of tax audit report (Form 3CA/3CB & 3CD)

- Increased scrutiny on incorrect reporting or under-reporting

- Penalty applicable under Section 271B for non-compliance

Forms Required for F&O Audit

- Form 3CA / 3CB – Audit report (3CA if accounts already audited, 3CB if not)

- Form 3CD – Detailed statement of financial and tax particulars

Due Dates for Tax Audit Filing

- Standard due date: 30th September (may be extended by government)

- Applicable for FY 2025–26 (AY 2026–27)

- Late filing may lead to penalties and compliance issues

Penalty for Non-Compliance

- Applicable under Section 271B

- Penalty = 0.5% of turnover

- Maximum penalty capped at ₹1,50,000