Futures & Options (F&O) Tax Audit

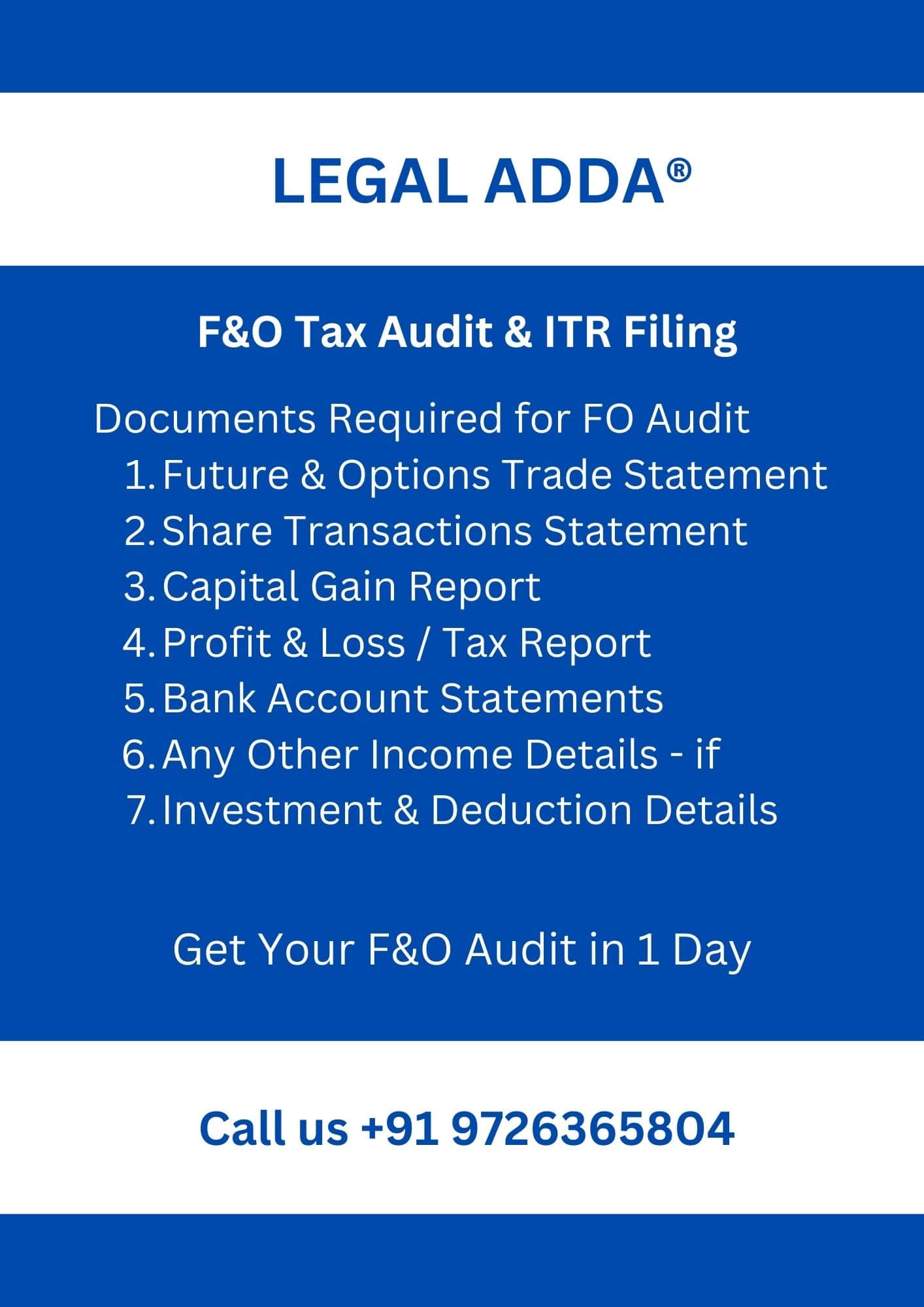

Looking for a Chartered Accountant who can handle your Futures & Options (F&O) Tax Audit and ITR filing with speed and accuracy? At Legal ADDA, we specialize in the audit of F&O trading clients and offer end-to-end compliance services for traders in the stock and share market. Whether you need an income tax audit, bookkeeping for F&O transactions, or online filing of Tax Audit Reports with ITR preparation, we provide it all — conveniently from a CA near you. Our one-stop solution covers everything from accounting and finalizing books of accounts (Profit & Loss A/c, Balance Sheet, etc.) to obtaining a DSC, Filing of the tax audit report (3CB-3CD) and filing your ITR. Get your F&O Tax Audit completed within 24 hours with our exclusive combo package — F&O Tax Audit + Accounting + Finalization + DSC + ITR Filing — all for just ₹14,000